Reinforcement Learning: The Next Frontier of AI in the Insurance Industry

Introduction

The insurance industry thrives on decisions — what to underwrite, how to price risk, when to settle a claim, and how to detect fraud. For decades, these decisions relied on static rules and historical data. But the world no longer stands still.

Enter Reinforcement Learning (RL) — an advanced branch of artificial intelligence that learns by interacting with the environment, continuously optimizing actions to achieve long-term goals.

In 2025 and beyond, RL is becoming a game-changer for insurance, powering dynamic pricing, proactive claims management, risk prevention through IoT, and portfolio optimization.

This blog explores how reinforcement learning works, its latest applications in insurance, and what it means for the future of adaptive, intelligent, and data-driven insurers.

🧠 What Is Reinforcement Learning (RL)?

Reinforcement Learning is a type of machine learning where an agent learns by trial and error in an environment, receiving feedback in the form of rewards or penalties.

Key concepts:

Agent: The decision-maker (e.g., pricing model, claims adjuster AI).

Environment: The world where it acts (insurance market, policyholder data, IoT sensors).

State: The current condition (customer risk profile, claim status).

Action: The decision taken (approve, deny, adjust price).

Reward: The outcome (profit, customer retention, reduced fraud).

Over time, the agent learns which actions maximize total reward — just like humans learning from experience.

Unlike supervised learning, which depends on labeled data, RL adapts in real time, making it ideal for dynamic markets like insurance.

🔍 The Rise of RL in Financial and Insurance Systems

According to McKinsey (2025), insurers using reinforcement learning for pricing and claims automation report up to 20–30% faster decision-making and 15% higher profit optimization compared to traditional AI methods.

Recent research from Stanford and MIT (2024–2025) highlights RL’s key advantages in:

Handling sequential decision-making (insurance renewals, claims lifecycles).

Adapting to non-stationary environments (changing risks, regulations).

Enabling continuous learning from live IoT and behavioral data.

As IoT adoption accelerates — with billions of connected devices providing real-time information — RL becomes the bridge between perception and intelligent action.

🌐 How RL Works in the Insurance Context

1. Underwriting and Dynamic Pricing

Traditional pricing uses static models trained on past data.

RL allows insurers to adjust premiums dynamically based on real-time behavior.

Example:

An auto insurer with telematics data can let an RL agent learn which combinations of driving behavior, weather, and location lead to claims. The model then rewards safe driving and penalizes risky actions, updating premiums automatically.

2. Claims Optimization

RL helps determine the optimal path to settle claims — balancing fraud risk, cost, and customer satisfaction.

Example:

The agent learns which claims should be fast-tracked, which need investigation, and which can be automated.

It continuously refines its policies to minimize loss while maximizing trust.

3. Fraud Detection

RL models can act as adaptive watchdogs, monitoring patterns of behavior.

Instead of static thresholds, agents learn evolving fraud tactics by simulating scenarios and adjusting detection strategies.

4. Portfolio and Risk Management

Reinforcement learning excels in multi-objective optimization — balancing return, risk, and compliance.

For investment-linked insurance products, RL agents can rebalance portfolios dynamically, similar to what hedge funds do with RL-based trading bots.

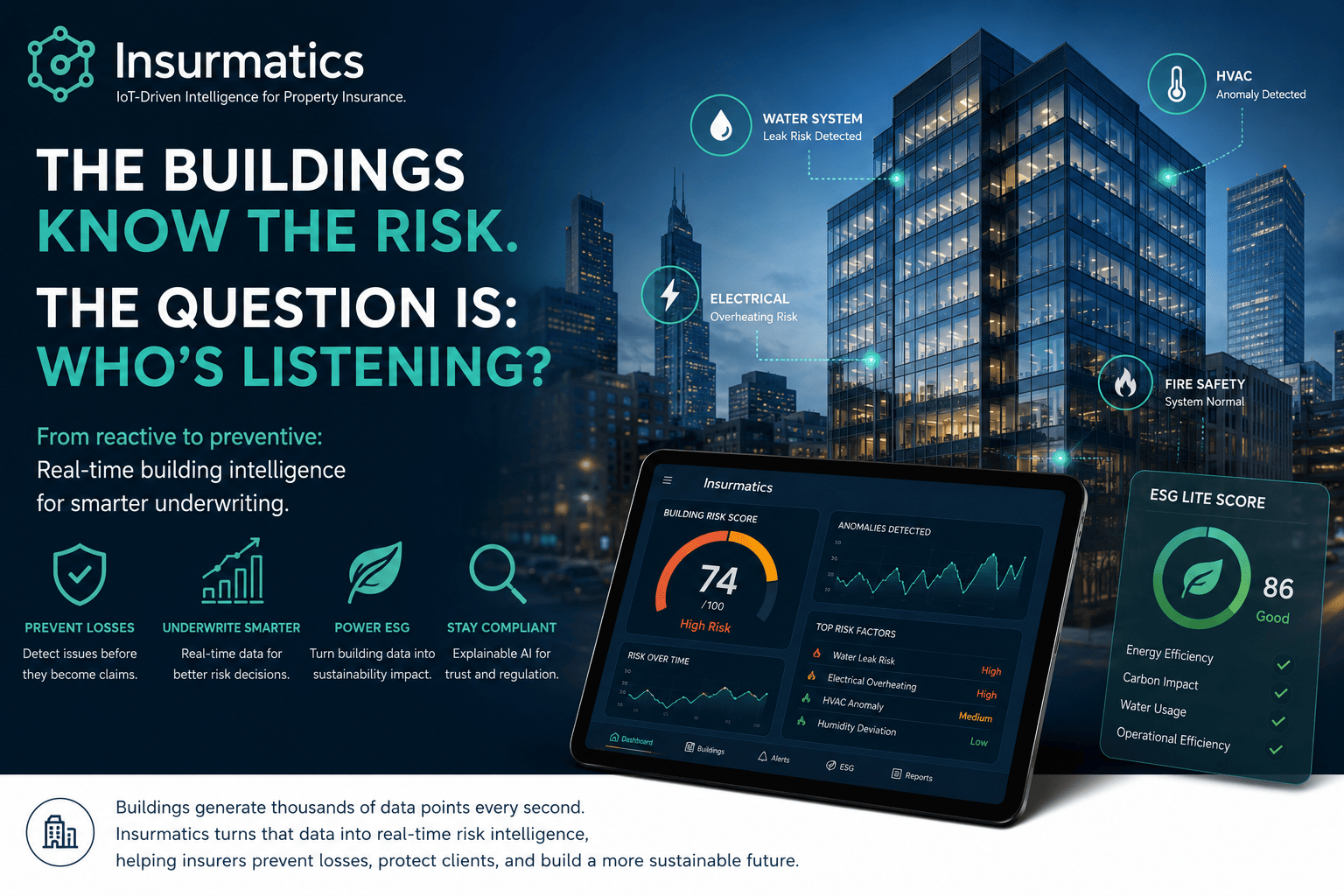

5. IoT-Driven Preventive Insurance

Connected sensors in buildings, vehicles, and health wearables generate real-time data. RL uses this data to prevent losses rather than react to them.

Example:

An RL agent linked to building sensors learns to predict pipe bursts or HVAC failures before they occur, alerting maintenance teams.

This transforms insurers from payers of loss to partners in prevention.

📊 Real-World Examples and Research

Progressive and Allstate have piloted RL-based telematics pricing, leading to more accurate and fair premiums.

Swiss Re is exploring RL for catastrophe risk modeling and capital optimization.

Ping An uses RL to optimize claims workflows and customer service chatbots.

DeepMind’s research (2024) on policy gradient methods now powers adaptive decision-making in finance and logistics — both directly applicable to insurance.

🚀 Global Trends Powering RL in Insurance (2025–2030)

1. Convergence of RL + IoT

With billions of IoT devices, RL agents are learning in continuous data loops, enabling micro-interventions before losses occur.

2. RL + Large Language Models (LLMs)

Next-gen LLMs (like GPT-5 and Gemini 2) integrate RL feedback loops to interpret complex insurance documents and regulatory frameworks while optimizing policy recommendations.

3. Edge RL Agents

Edge computing allows RL models to operate locally on IoT gateways, enabling instant decisions even without internet connectivity — vital for real-time risk prevention.

4. RL for ESG Optimization

RL is increasingly used to optimize ESG portfolios and carbon footprints, balancing sustainability with profitability.

5. RL as a Service (RLaaS)

Cloud providers now offer ready-made RL environments for insurers to test strategies safely — like AI “sandboxes” for decision-making.

⚙️ Challenges Ahead

Data Volume & Quality: RL needs high-quality, continuous feedback data — IoT solves this but raises integration complexity.

Explainability: Regulators demand transparency; RL’s dynamic policies can appear “black-box.”

Ethical & Regulatory Boundaries: Need safeguards to prevent discriminatory pricing or claim handling.

Computational Power: Training RL agents can be hardware-intensive (requiring GPUs/TPUs).

Cultural Adoption: Organizations must trust automated agents and redefine roles around them.

✅ Conclusion

Reinforcement Learning is redefining the insurance value chain — shifting the industry from reactive claims and static pricing to adaptive, real-time decision-making.

As IoT expands and AI hardware becomes more powerful, RL stands as the missing intelligence layer that connects data, prediction, and action.

From smart risk prevention to fairer pricing to automated claims, RL enables insurers to learn, adapt, and lead in a world of constant change.

📩 Interested in exploring AI or IoT pilots? Contact [email protected]

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Say goodbye to your low online sales rate!

Why is RL better than traditional AI in insurance?

A1: Traditional models are static — RL continuously learns and improves, enabling adaptive pricing, claims, and risk prevention.

Q2: Is RL already used by major insurers?

A2: Yes — leading firms in the US, EU, and China are piloting RL in underwriting, telematics, and claim settlement optimization.

Q3: How does RL connect with IoT?

A3: IoT provides the environment; RL provides the decision intelligence — together enabling autonomous, real-time insurance operations.

Q4: Does RL replace human underwriters?

A4: No — it augments them. Humans set goals and guardrails; RL executes decisions faster and smarter.

Q5: What skills do insurers need for RL adoption?

A5: Data engineering, model governance, and reinforcement learning expertise — along with an open culture for experimentation.