Europe Opens the Door for Faster AI Innovation — A Strategic Guide for Insurers

Introduction

The European Union’s AI Act and General Data Protection Regulation (GDPR) have been global reference points for digital governance. But as 2025 unfolds, both frameworks are being scaled back and re-shaped in response to innovation pressure, geopolitical competition, and the explosion of generative AI.

According to recent coverage by and , European lawmakers have signaled a shift from rigid control to adaptive regulation — relaxing certain AI risk-classification rules and softening GDPR enforcement mechanisms to encourage startups and enterprise adoption.

For the insurance sector, this change marks both a challenge and an opportunity. While compliance burdens may ease, expectations for responsible AI and data governance remain high. This article explores the new landscape, how it affects insurers, and provides a practical roadmap for navigating it.

⚖️ The Policy Shift: From Restriction to Adaptation

1. The AI Act: Light-Touch Implementation

The original AI Act (approved in early 2024) classified AI systems into “unacceptable,” “high,” “limited,” and “minimal” risk categories. However, regulators faced pushback from both industry and member states over feasibility.

The revised version (late 2025):

Softens “high-risk” obligations for enterprise analytics and generative models.

Introduces voluntary compliance codes for sectors like insurance and finance.

Focuses enforcement on foundation models and AI used in biometric or surveillance contexts.

Expands “regulatory sandboxes” — safe testing zones where insurers and fintechs can deploy AI systems with reduced penalties.

2. GDPR 2.0: Data Portability and Enforcement Lightening

The European Commission’s proposed GDPR adjustments aim to reduce friction for innovation:

Streamlined cross-border data transfer approvals.

Simplified consent management for anonymized or synthetic data.

Emphasis on risk-based rather than blanket compliance.

Fewer fines for first-time technical violations, shifting toward cooperative correction.

3. The Motivation Behind Scaling Back

Europe is responding to a competitive reality: the U.S. and Asia have surged ahead in AI investment. The goal is to make Europe a center for “trustworthy innovation,” not just regulation.

🌍 Implications for the Insurance Sector

1. Easier AI Experimentation

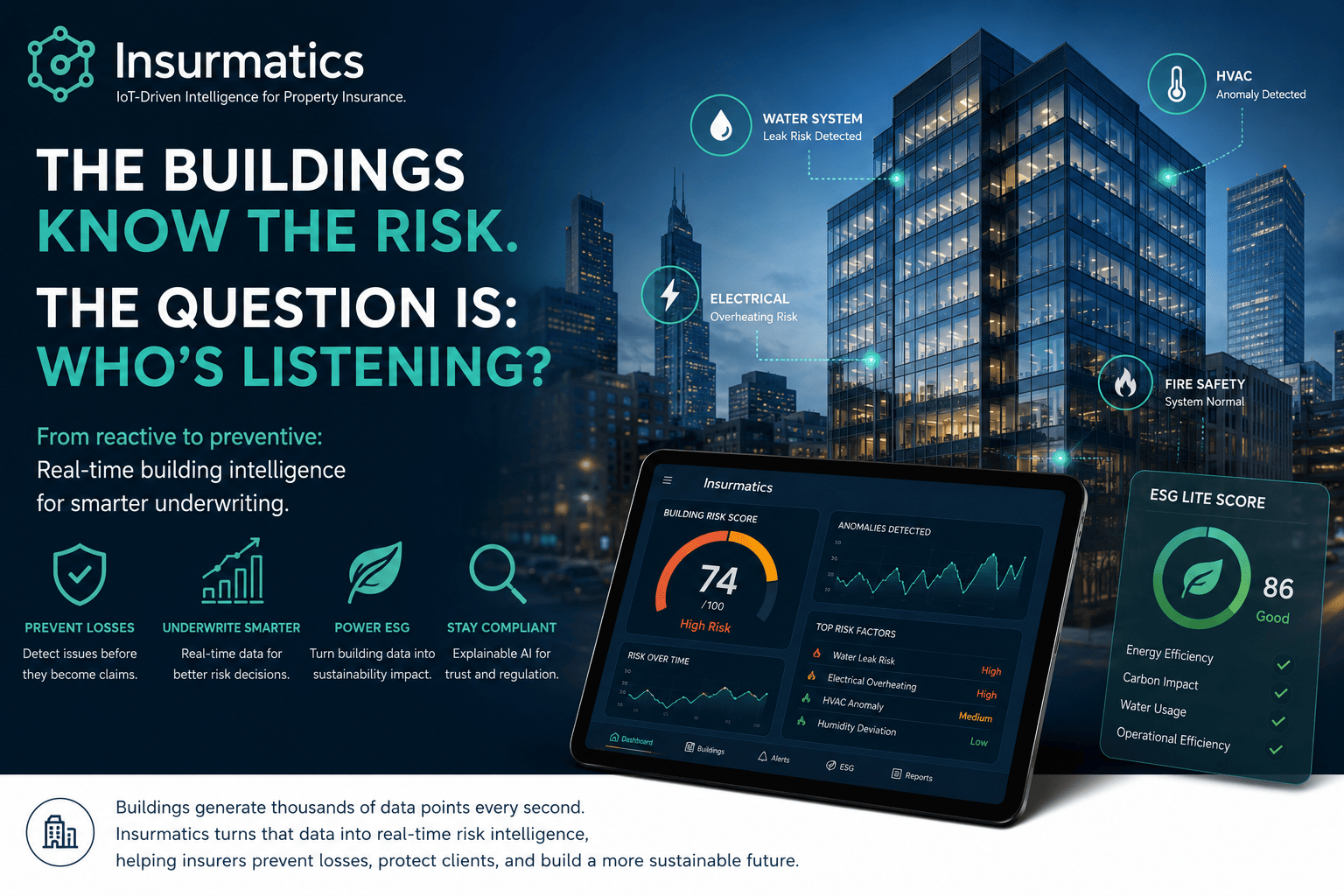

Insurers can now train and deploy generative and predictive models (e.g., for claims analysis or underwriting) under clearer, less restrictive rules — especially in sandboxes.

2. IoT Data Integration

Relaxed data portability rules allow cross-system integration (e.g., between telematics, BMS sensors, and ESG reporting). This paves the way for real-time risk scoring.

3. Reduced Compliance Cost

Small and mid-size insurers and brokers can scale AI without the need for large data-protection teams.

4. Increased Accountability

While regulation is lighter, public and ethical scrutiny intensifies. Misuse of AI (biased models, unfair pricing) can still destroy trust and trigger reputational risk.

5. Cross-Border Harmonization

Insurers operating across Europe will find fewer legal discrepancies between countries, simplifying multinational operations.

🧭 Roadmap for Insurers: How to Adapt and Lead

Step 1: Reassess Your AI Risk Framework

Re-evaluate internal AI projects under the new “risk-based” lens.

Document model transparency, fairness, and explainability — even if not mandated.

Create an AI Register: list all algorithms affecting underwriting, pricing, claims, or ESG scoring.

Step 2: Leverage Regulatory Sandboxes

Participate in national or EU-level sandboxes to test new models with reduced penalties.

Collaborate with innovation hubs (e.g., Lithuania, Estonia, Netherlands, Spain).

Use sandbox results to influence future compliance design.

Step 3: Build Privacy by Design

Even with relaxed GDPR rules, privacy remains central to trust.

Continue using data minimization, pseudonymization, and federated learning.

Adopt privacy-enhancing computation (PEC) — such as differential privacy or homomorphic encryption.

Step 4: Strengthen AI Governance

Form an AI Oversight Committee including legal, technical, and actuarial experts.

Use AI Ethics checklists based on ISO/IEC 42001 (AI management systems).

Align with the OECD AI Principles — transparency, accountability, robustness.

Step 5: Integrate ESG & Data Ethics

Incorporate ESG factors (carbon, social fairness, governance transparency) into data pipelines.

Publish annual AI & Data Ethics Reports — a proactive trust signal.

Step 6: Prepare for the Next Wave — AI Hardware & Edge Computing

Invest in on-premise or hybrid AI hardware infrastructure for real-time analytics.

Use edge AI chips to analyze IoT risk data locally, reducing privacy exposure.

📈 Opportunities Emerging from the Policy Shift

Faster Innovation Cycles

Insurers can iterate models rapidly without legal paralysis.

Cross-Sector Data Partnerships

Easier data exchange with mobility, energy, or property sectors.

Expansion into New Risk Domains

AI can now model climate, ESG, and operational risks with greater flexibility.

More Room for Generative AI

AI can automate claims narratives, generate risk reports, and enhance client communication.

⚠️ Risks That Remain

Ethical Drift: Lighter oversight may embolden misuse of AI for exclusionary pricing.

Consumer Mistrust: Perceived deregulation could reduce confidence in “fair AI.”

Fragmentation Risk: Member states could still diverge in local interpretation.

Cyber Vulnerability: Relaxed data transfer rules increase exposure if not mitigated.

Conclusion

Europe’s decision to scale back its landmark privacy and AI laws represents a pivotal recalibration — from restriction to resilience.

For the insurance sector, this creates space for innovation in risk modeling, ESG reporting, and customer experience, while reinforcing the moral duty to uphold transparency, fairness, and privacy even without regulatory compulsion.

Those who adapt fastest — balancing compliance with experimentation — will lead the next generation of AI-enabled, data-driven insurers.

📩 To explore AI and data compliance strategies tailored for insurance, contact [email protected].

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Say goodbye to your low online sales rate!

Q1: Does scaling back mean Europe is abandoning data privacy?

A1: No. The shift aims for flexibility, not deregulation. Core GDPR principles remain; enforcement is simply more adaptive.

Q2: Can insurers now use generative AI more freely?

A2: Yes, particularly in sandboxes or low-risk applications like document drafting, client chatbots, and ESG summaries — provided transparency and human oversight are maintained.

Q3: How will this affect cross-border insurance operations?

A3: Positively. Harmonization and portability rules simplify compliance for multinational insurers operating in multiple EU jurisdictions.

Q4: Will data ethics still matter to regulators?

A4: Absolutely. Even with relaxed laws, ethical AI is becoming a business differentiator — influencing brand reputation and ESG scoring.

Q5: What concrete steps should insurers take today?

A5: Conduct a compliance audit under new guidelines, participate in sandboxes, implement internal AI governance, and maintain transparent reporting.