How Property Insurance Companies Can Use AI Agents and IoT for Good: A Roadmap for Smarter, Fairer, and Safer Coverage

🌍 Introduction

Property insurance is undergoing a quiet revolution. While extreme weather, aging infrastructure, and rising claim costs challenge the sector, new technologies — AI agents and IoT (Internet of Things) — are reshaping what insurers can achieve.

These tools are not only driving efficiency and profitability but are becoming essential to social good, resilience, and climate adaptation.

AI agents, when combined with IoT, empower insurers to move from to . They make insurance more transparent, sustainable, and equitable for both policyholders and communities.

In this article, we’ll explore how property insurers can:

Use AI agents and IoT for prevention and fairness,

Implement them through a step-by-step roadmap, and

Stay aligned with the latest global trends and ethical frameworks.

🤖 What Are AI Agents in Insurance?

AI agents are autonomous, intelligent systems capable of perceiving data, reasoning, and acting toward defined goals — with or without direct human supervision.

When embedded in IoT networks, AI agents can:

Monitor sensor data from buildings in real time,

Detect anomalies such as leaks, temperature spikes, or equipment stress,

Recommend or execute actions, like shutting valves or alerting maintenance,

Learn from outcomes to improve future predictions.

In property insurance, this means turning reactive workflows into continuous risk management ecosystems.

💡 How IoT Complements AI Agents

IoT provides the senses — sensors and connected devices.

AI agents provide the brain — reasoning, prioritization, and decision-making.

Together they create a closed feedback loop:

Sense → Think → Act → Learn → Report.

Examples include:

Smart water sensors that automatically shut off valves when leaks occur.

Environmental monitors that adjust ventilation to reduce mold or humidity.

Predictive fire prevention using temperature, smoke, and air quality analytics.

For insurers, this isn’t just technology — it’s a new business model centered around prevention, personalization, and partnership.

📈 The Global Trend: From Payout to Prevention

Swiss Re (2024) reports that climate-related property losses have increased by 40% in five years.

Capgemini (2025) highlights that 80% of insurers now see IoT as essential to their sustainability and risk goals.

McKinsey (2025) projects that AI-driven property risk prevention could reduce claims costs by up to 25%.

In 2025, the convergence of AI + IoT + ESG has become a defining trend in insurance innovation. Regulators and investors now demand proof of proactive resilience, not just reactive compensation.

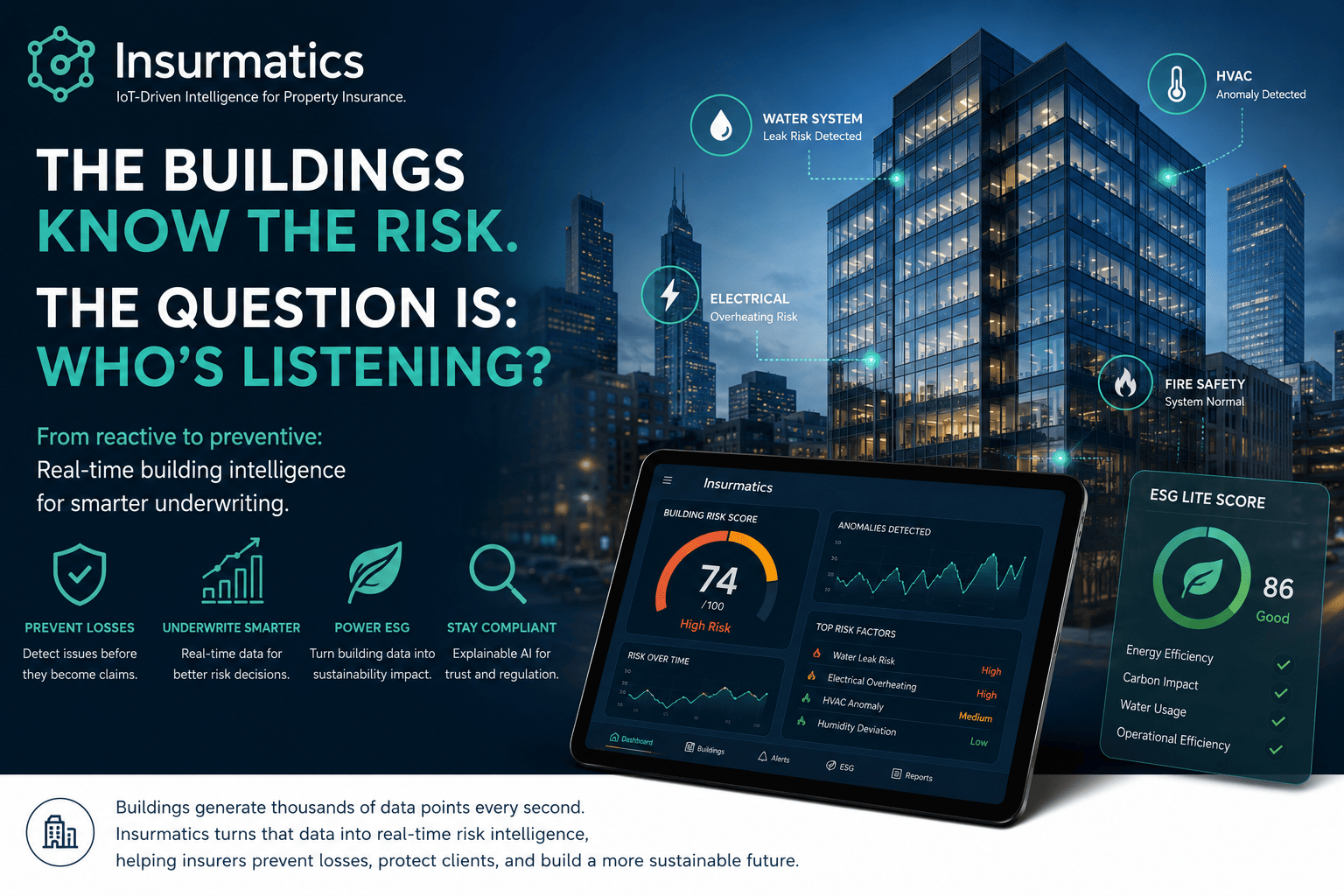

🔧 Core Benefits of AI-Agent + IoT Integration

| Area | Value for Insurers | Value for Society |

|---|---|---|

| Loss Prevention | Early detection of leaks, fires, equipment failures. | Reduced damages, safer homes and workplaces. |

| Operational Efficiency | Automated claims validation and maintenance scheduling. | Faster service and transparent settlements. |

| Fair Pricing | Real-time data enables usage-based premiums. | More affordable and personalized coverage. |

| ESG & Compliance | Automated energy and CO₂ reporting via IoT sensors. | Accelerates sustainability commitments. |

| Customer Trust | Real-time engagement and alerts strengthen relationships. | Policyholders feel supported, not penalized. |

🧭 Implementation Roadmap

Here’s a five-phase roadmap for property insurers ready to act:

Phase 1 — Strategy & Vision

Define goals: prevention, sustainability, customer engagement, or new products.

Align with corporate ESG, compliance (CSRD, TCFD), and risk frameworks.

Appoint an internal AI + IoT Innovation Team.

Phase 2 — Data Infrastructure & IoT Integration

Select IoT domains: water, HVAC, fire safety, structural integrity, environmental sensors.

Adopt open protocols (MQTT, Modbus, BACnet) for interoperability.

Deploy secure gateways for data ingestion, edge processing, and API access.

Phase 3 — AI Agent Deployment

Introduce AI agents that interpret IoT data in real time.

Train models for anomaly detection, event prediction, and ESG metric aggregation.

Integrate with insurer systems (CRM, claims, underwriting).

Use feedback loops so AI agents learn from outcomes.

Phase 4 — Customer Ecosystem Integration

Offer connected insurance products (e.g., smart property bundles).

Provide customers with apps or dashboards for alerts, analytics, and tips.

Reward risk-reducing behavior through dynamic pricing or credits.

Phase 5 — Scaling and Continuous Improvement

Expand to new property classes: commercial, industrial, municipal.

Automate ESG data reporting for investors and regulators.

Use insights for new risk models and parametric insurance products.

🔒 Ethical and Social Dimensions: “AI for Good”

AI agents and IoT must serve people and planet, not just profits.

Insurers can use these technologies to:

Promote inclusion: Offer lower premiums for communities investing in resilience.

Support climate adaptation: Incentivize retrofits, water-saving, and energy efficiency.

Enhance transparency: Explain AI-driven pricing decisions.

Protect privacy: Adopt clear data governance and consent frameworks.

When applied responsibly, AI + IoT make insurance not only more efficient — but more humane and sustainable.

🧩 Example Use Cases

1. Water Damage Prevention (Residential & Commercial)

IoT leak sensors trigger AI-agent alerts → cut water supply.

Claim reduction up to 30%, especially in multi-floor buildings.

2. Fire Risk Management

AI agents monitor humidity, temperature, and electrical load.

Prevent fires in data centers or old residential blocks.

3. ESG and Green Building Verification

AI agents track energy, CO₂, and comfort KPIs for regulatory reporting.

Automates CSRD-aligned sustainability scoring.

4. Real-Time Property Valuation

Continuous IoT monitoring refines risk-based property valuation models.

5. Automated Claims Validation

Edge AI cameras verify incidents; AI agents cross-check with IoT evidence → faster settlements.

🏗️ Technical Architecture Overview

IoT Layer: Sensors (energy, water, IAQ, motion).

Edge Layer: Local AI inference for latency-sensitive events.

Cloud/Platform Layer: Centralized data lake and analytics engine.

AI Agent Layer: Autonomous decision-making, reasoning, and action planning.

Application Layer: Dashboards, APIs, reports, ESG compliance exports.

This architecture supports scalable, secure, and audit-ready insurance innovation.

🔄 Future Outlook: Autonomous Insurance

By 2030, property insurers will evolve into autonomous ecosystems, where:

AI agents act as , evaluating risks continuously.

IoT data feeds and .

ESG outcomes become part of the , not just disclosure.

Insurers who start now will lead the market in trust, resilience, and sustainability.

✅ Conclusion

AI agents and IoT represent the next frontier of property insurance — where prevention, transparency, and sustainability redefine the value chain.

From smart leak detection to ESG compliance automation, these technologies turn insurers into active partners in risk reduction and social resilience.

The roadmap is clear: start small, integrate deeply, scale ethically.

Insurers who act today won’t just protect properties — they’ll protect the future.

📩 To explore AI + IoT pilot programs or co-develop an ESG-driven insurance framework, contact: [email protected]

Make Your Business Online By The Best No—Code & No—Plugin Solution In The Market.

30 Day Money-Back Guarantee

Say goodbye to your low online sales rate!

Q1: Why should property insurers invest in AI and IoT now?

A1: Because prevention-based models are replacing reactive claims. Early adopters achieve cost savings, improved customer retention, and ESG leadership.

Q2: What’s the biggest technical challenge?

A2: Integrating diverse IoT protocols and ensuring data quality for AI training. Using open standards and modular architectures helps.

Q3: Can AI agents operate autonomously in risk decisions?

A3: Yes, within limits. Human oversight is essential for ethical and legal compliance, but automation can handle >80% of operational tasks.

Q4: How does this align with sustainability goals?

A4: IoT data supports measurable ESG performance, while AI optimizes energy use and minimizes losses, directly aiding net-zero strategies.

Q5: What ROI can insurers expect?

A5: Typical pilots show 20–30% claim cost reduction, 15–20% operational efficiency, and faster ESG reporting cycles.